Cosmetic Matching in Colorado…Yes, But…..

With the recent circuit court decision in the Bertisen v. Travelers Home and Marine Insurance Company, there has been a lot of discussion around cosmetic matching requirements in Colorado. While the case did provide some light on the court’s opinion of definitions in a policy and how that applies to matching, the real determination on whether matching is required still comes down to language in each policy in effect when a covered loss occurs.

In the Bertisen case, Judge Wang effectively said that the language in Travelers policy did not clearly state that the policy insures down to the lowest invisible unit, in that instance, a single roofing tile. Further, the Travelers policy did not define “like kind and quality for like use.” Because the tiles were no longer made, and the policy insures the dwelling, rather than individual components, she determined that the policy could be reasonably interpreted to account for cosmetic matching.

Ultimately, this matching decision is welcome news for insureds in Colorado, many of whom have antiquated roofs, windows, and siding currently installed on their homes. The decision also comes after a Colorado season of increased storm activity in 2023. Many contractors and Colorado insureds have viewed this as an opportunity to pursue full replacements of these systems due to hail in instances where carriers would have traditionally proposed a repair with mismatched material. While there is certainly opportunity, contractors and insureds need to have their policies reviewed before pursuing a potentially fruitless claim.

Colorado Hailstorms in 2023

There is no shortage of properties that were damaged by the Colorado hail storms in 2023, but not all of the policies in effect at those properties will support arguments for cosmetic matching. I have been seeing more and more examples of policy language that is expressly intended to prevent affording coverage for matching. A couple of examples I have come across on some recent claims that I have reviewed;

Allstate’s “Colorado Amendatory Endorsement – AVP257-2”

This endorsement is not new and has been in most (if not all) Colorado homeowners policies since 2014. Effectively, any Allstate policies with this endorsement remove the insured’s ability to argue matching in instances where the damaged material is no longer made or cannot be reasonably matched.

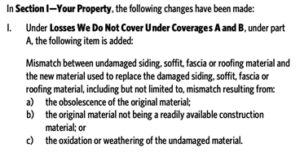

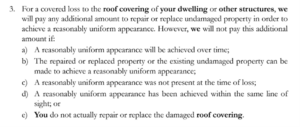

Pure’s “Hail Coverage and Loss Settlement” Endorsement

This endorsement is unique as it states that the policy covers cosmetic matching, subject to 5 conditions. The endorsement gives the carrier five “outs” that are common situations, especially c and d. Previous repairs are relatively common, especially on tile roofs in Colorado, and usually do a good job of demonstrating how repairs are not effective in achieving a reasonable uniform appearance. Line of sight is subjective and can be interpreted in several ways.

American Family has also started to place “matching exclusions” in their policies, for the express purpose of limiting coverage for damages down to the smallest divisible unit on a property.

This is where an experienced Colorado Public Adjuster can assist in qualifying and consulting on the practical implications of the policy language in effect at the date of loss on the claim outcome. A Denver Public Adjuster with knowledge of the conditions in the policy that produced the court order in the Bertisen case, an understanding of what materials are no longer made or cannot be matched, and how hail damage presents itself on those materials will be able to objectively inform contractors and insureds on whether they can argue for cosmetic matching in their claim. As work continues repairing damage from the 2023 Colorado hail season and we enter the 2024 season, it is important to review all the pertinent information before spending time and money pursuing a claim. Prime Adjustments has the experience and knowledge necessary to assist policyholders and their contractors in making the best decisions when it comes to their storm damage claims.